Editor’s Note: The following is Part 2 of my 3 part series “The Freelancer’s Guide to Managing Your Money in the ‘Gig Economy’ (and Surviving Global Pandemics).”

Here’s what’s covered in all three parts:

Part 1: Creating Your ‘Triage Budget’ & Understanding Cash Flow

→ Part 2: How to Generate Income (Even If You Can’t Find Work)

Part 3: Reorganizing Your Finances For Stress-Free Unemployment (publishing soon)

DISCLAIMER: The following is all information based off my own research from the interwebs (with links verifying all claims) as well as in-depth conversations with my own accountant and bookkeeper. I am not a licensed CPA, bookkeeper, or accountant of any kind. You should do your own due diligence with the resources provided to verify the claims below and proceed accordingly at your own discretion. As new information (rapidly) becomes available I will update this post accordingly.

In the last week you’ve probably read an article or two (or fifty) about freelancers like us FINALLY getting access to unemployment benefits, the potential to get an SBA loan to cover payroll for you or your team, and other various (confusing) options to keep us afloat during this pandemic.

But then perhaps you tried to apply for unemployment (or your $10k grant…which them became your $1k grant…which you then had to apply for again….), and it was an unmitigated disaster.

As you have no doubt already heard, the federal government recently passed the CARES Act (the Coronavirus Aid, Relief, and Economic Security Act), a $2 trillion dollar package that is the largest stimulus in American history.

That’s great…in theory. If and when it actually works.

And when it does work, you no doubt have questions.

When do I get MY cut?

How much do I get?

What am I eligible for?

How do I apply?

Where do I apply?

The short answer to all of these questions is:

It’s complicated.

Like playing a game of 7 dimensional chess in The Matrix buried 3 layers deep inside someone’s dream using Inception complicated.

Just when you thought your application was processed…not so much.

If you’ve been waiting to apply until the government releases a step-by-step resource to help you make sense of the various options you’re eligible for…keep dreaming. They’ve got tens of millions of applications to screw up process and hundreds of millions of stimulus checks to cut.

The government isn’t going to do the work for you and make sure you get the money you’re owed.

We’re on our own figuring this out and getting paid.

I’m guessing you have no interest in spending two or more full days sifting through hundreds of government documents, articles, briefs, and constantly staying up-to-date with the latest stimulus changes and regulations, right?

Luckily I’ve done all the hard work for you (while y’all binged Tiger King).

You see, I want you to be as effective with your time, energy, and attention as possible (global pandemic or otherwise), and trying to make sense of the madness that is the CARES Act should not be on your to-do list with kids that need home-schooling, Zoom calls that need Zooming, closets that need reorganizing, and episodes of Ozark that desperately require binging.

I want you to be able to spend just a few minutes reviewing your options below so you can make educated, step-by-step decisions about what to apply for and when.

To be honest…even after working through all 4 sections of this article, this process still won’t be easy.

In fact…this is gonna SUUUUUUUUUUUCK.

But if you maximize the various stimulus options available to you, you’ll probably make a fairly significant hourly wage when you average out your time spent applying and the overall money you receive in return.

Ready to dive in? Let’s get started then.

[TABLE OF CONTENTS]

Section 1: Your Government Stimulus Check

Section 2: The Economic Injury Disaster Loan (EIDL), aka The ‘SBA Disaster Loan’

Section 3: The Paycheck Protection Program (PPP)

Section 4: Filing For Unemployment Insurance (UI)

Section 5: Other Ways to Earn Income

Section 1: Your Government Stimulus Check

As you no doubt already know, the most immediate form of relief everyone will (potentially) receive is government stimulus checks. The eligibility varies based on your income and whether or not you have children. Further details outlining whether or not you should expect a check are below.

Income Potential:

Depending on the criteria outlined below, anywhere between $0 and $5k+ (depending on number of kids in your family).

The most important question to ask first:

Do I need to apply?

No need to apply. This is calculated automatically based on the adjusted gross income* on your 2019 tax returns (if you’ve already filed) or your 2018 tax returns (if you haven’t filed 2019 yet).

*Note: Your Adjusted Gross Income (AGI) is line 8b of your Federal 1040 tax form.

Simply put…don’t waste another minute on your government stimulus. It will take care of itself and show up in your account when it shows up.

You should focus all of your time, energy, and attention on the other income options below.

How much will my stimulus check be?

According to the New York Times (and verified by countless other sources)1:

- Single adults with Social Security numbers who have an adjusted gross income of $75,000 or less will get the full amount.

- Married couples with no children earning $150,000 or less will receive a total of $2,400.

- Taxpayers filing as head of household will get the full payment if they earned $112,500 or less.

- Above those income figures, the payment decreases until it stops altogether for single people earning $99,000 or married people who have no children and earn $198,000. According to the Senate Finance Committee, a family with two children will no longer be eligible for any payments if its income surpassed $218,000.

- Households with children will also receive $500 each for each child if the parent’s income qualifies for these payments and if the child is under the age of 17.

Here are three groups of people who WON’T get a stimulus check

How many checks will I receive?

For now you will only receive one check. This will no doubt evolve, however, as current events change.

When will my stimulus check arrive?

UPDATE (04.15.20 10:28 am): There is now an IRS site that lets you check up on the status of your refund.

Just don’t get your hopes up quite yet…..

Let’s be honest…this as a rapidly moving target and nobody really knows for sure. You could see a check as soon as April 9th…or you might have to wait months.

According to Treasury Secretary Steven Mnuchin:

“If we have your information, you’ll get [your stimulus check] within two weeks. Social Security, you’ll get it very quickly after that. If we don’t have your information, you’ll have a simple web portal. We’ll upload it. If we don’t have that, we’ll send you checks in the mail.”

According to an internal IRS memo reviewed by The Washington Post, stimulus payments will begin arriving in people’s bank accounts as soon as April 9th. Most people who get their IRS refunds via direct deposit should have their stimulus checks by mid-April.

The giant disclaimer is that if you don’t have direct deposit set up, paper checks will not start going out until April 24th. The IRS plans to send out 5 million checks per week (moving up based on income threshold starting at $10k or less). They intend for all checks to be delivered by September 11th2.

Section 2: The Economic Injury Disaster Loan (EIDL) aka The ‘SBA Disaster Loan’

If your sole method of earning income is as a full-time W2 employee, you can skip this section and go directly to Section 4.

Otherwise, if you are a small business, sole proprietor, freelancer, or independent contractor, applying for your EIDL grant is where you need to focus all of your time, energy, and attention ASAP.

Income Potential:

Starting at a $1-$10k grant all the way up to $2+ million dollars in business loans

Who is eligible?

As mentioned above, you cannot apply for the SBA Disaster Loan if you earn your income solely via W-2 income as an employee.

The following people can apply:

- All small businesses (S-corps, C-corps, LLC’s)

- Sole proprietors (what is a sole proprietor according to SBA?)

- Independent contractors (what is an independent contractor?)

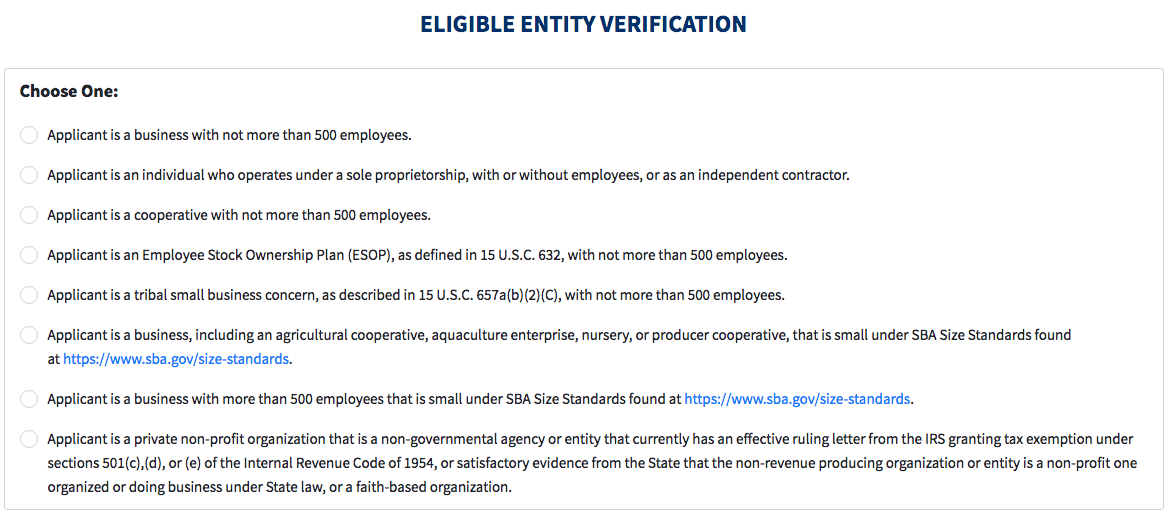

Here is a screenshot directly from the SBA Disaster Loan Application regarding eligibility

Do I need to apply?

Yes, you must apply for the SBA Disaster Loan to receive any money.

When can I apply?

NOW. IMMEDIATELY. ASAP. Like seriously, stop reading this article and apply now. It takes less than 5 minutes.

» » Click here to apply for your (up-to) $10,000 grant (directly from SBA)

ALERT: If you heard about the SBA Disaster Loan right after it came out and applied before April 1st (like I did), YOU HAVE TO APPLY AGAIN. (Here’s more info)

Here’s all the info you’ll need to have prepared (it ain’t much):

- Your EIN or SSN

- Your gross income for 2019

- Your cost-of-goods sold for 2019

What benefits are available?

UPDATE (04.08.20 11:03am): No surprises here…the government has moved the goal posts since publishing their original guidelines. The NEW guidelines state that you can apply for UP TO a $10,000 grant, with $1000 per employee.

Here’s even more info about the SBA loan chaos in progress

All qualified businesses, sole proprietors, and independent contractors will receive an “up-to” $10,000 grant based on the number of employees. Not a loan – a grant.

FREE. EFFIN’. MONEY.

Beyond that, the EIDL loan program gets a lot more difficult.

According to the SBA3:

- The Economic Injury Disaster Loan Program (EIDL) can provide up to $2 million of financial assistance (actual loan amounts are based on amount of economic injury) to small businesses or private, non-profit organizations that suffer substantial economic injury as a result of the declared disaster, regardless of whether the applicant sustained physical damage.

- An EIDL can help you meet necessary financial obligations that your business or private, non-profit organization could have met had the disaster not occurred. It provides relief from economic injury caused directly by the disaster and permits you to maintain a reasonable working capital position during the period affected by the disaster. EIDLs do not replace lost sales or revenue.

- The SBA can provide up to $2 million in disaster assistance to a business. The $2 million loan cap includes both physical disaster loans and EIDLs. There are no upfront fees or early payment penalties charged by SBA. The repayment term will be determined by your ability to repay the loan.

- The annual interest rate is 3.75% for businesses, 2.75% for non-profits, and the loan term is up to 30 years4

When will I get my money?

An excellent question…

According to several sites and resources, you could receive your grant in as little as three days (after your application has been processed).

But I’m not holding my breath.

There are numerous unverified reports floating around right now that not a single person has received a dollar yet, which has led to the creation of the hashtag #EIDLHOAX.

Until I start to read about people actually seeing money in the bank, I’m not counting on any stimulus to cover short term cash flow, and I’m strategizing alternatives (e.g. emergency funds, slashing expenses, etc).

If/when the money does arrive in my bank account, then I’ll allocate it accordingly.

Section 3: The Paycheck Protection Program (PPP)

Between your stimulus check and your “up-to” $10,000 grant, if I’ve gotten your hopes up that the Paycheck Protection Plan will provide even more financial assistance with little investment of time applying… you’ll need to severely curb your enthusiasm.

As of publishing this article, the Paycheck Protection Plan rollout has been a Complete. Unmitigated. Disaster.

Wells Fargo has already stopped taking applications

Big banks are favoring existing customers over others applying

That having been said, if/when they work out the many technical snafus that one would expect with the largest government stimulus program in history, there are many benefits if you do qualify.

If your sole method of earning income is as a full-time W2 employee, you are not eligible for the PPP and can go directly to Section 4.

Income Potential:

Depends on existing payroll, but potentially up to $10 million

Who is eligible?

As mentioned above, you cannot apply for the Paycheck Protection Program if you earn your income solely via W-2 income as an employee.

The following can apply:

- All small businesses (S-corps, C-corps, LLC’s) in operation as of February 15th, 2020

- Sole proprietors (what is a sole proprietor according to SBA?)

- Independent contractors (what is an independent contractor?)

- Self-employed individuals

Where do I apply?

Where this gets tricky is that unlike the SBA Disaster Loan, you apply for PPP loans with individual banks, not via SBA or the US Treasury.

Unfortunately many banks are making this process exceedingly difficult as well as excluding non-customers in many circumstances. Hopefully these issues will be resolved (or regulated) soon. My best advice for now would be to apply through whomever you do your business banking with.

» Click here for the Payroll Protection Plan Application Form*

*Keep in mind many banks will use their own application forms. This should be used as a general guideline.

When can I apply?

- Small businesses and sole proprietorships can apply now (as of April 3rd)

- Independent contractors and self-employed individuals (i.e. those who only receive 1099 income) can apply as of April 10th

How does it work?

The PPP is far more complex than EIDL. It essentially allows you to do as the name suggests: Protect your companies’ payroll. This only includes your employees on payroll and does NOT include independent contractors.*

And the kicker is, under certain circumstances this loan can be forgiven.

*Disclaimer: This could all change, as could every other detail below…like I said….rapidly moving target.

Here are the basics:

- The maximum loan size is $10 million

- If you were in business as of February 15, 2019 – June 30, 2019, **the max loan is equal to 2.5x the average monthly payroll costs of the 12 months prior to your application.**

- If you were not in business between February 15, 2019 – June 30, 2019, the max loan is equal to 2.5x the average monthly payroll costs between January 1, 2020 and February 29, 2020.

Features include:

- No fees

- No prepayment penalties

- No business collateral or personal guarantee required

- Loan forgiveness for eligible payroll, mortgage interest, rent and utilities during the covered eight-week period after origination

- Payments are deferred for six months

Eligible payroll expenses would INCLUDE:

- Compensation (salary, wage, commission, or similar compensation, payment of cash tip or equivalent)

- Payment for vacation, parental, family, medical, or sick leave

- Allowance for dismissal or separation

- Group health care benefits, including insurance premiums

- Retirement benefits

- State or local tax assessed on the compensation of employees

Here’s is what is EXCLUDED:

- Employee/owner compensation in excess of $100,000

- Taxes imposed or withheld under chapters 21, 22, and 24 of the IRS code

- Compensation of employees whose principal place of residence is outside of the U.S.

- Qualified sick and family leave for which a credit is allowed under sections 7001 and 7003 of the Families First Coronavirus Response Act

Here are the criteria for your PPP loan to be forgiven5:

- 75 percent of the PPP loan is supposed to be used to fund payroll and employee benefits costs.

- The remaining 25 percent can be spent on:

- Mortgage interest payments

- Rent and lease payments

- Utilities

- If you stick to these guidelines, you’ll be able to have 100% of the loan forgiven (effectively turning it into a tax-free grant).

- In the 8 weeks following your loan signing date, all expenses related to the following can be forgiven:

- Payroll—salary, wage, vacation, parental, family, medical, or sick leave, health benefits

- Mortgage interest—as long as the mortgage was signed before February 15, 2020

- Rent—as long as the lease agreement was in effect before February 15, 2020

- Utilities—as long as service began before February 15, 2020

- You’ll need to keep your records and have accurate bookkeeping to prove your expenses during the loan period. You will also need to have spent 75% of your loan on payroll in order to qualify for loan forgiveness.

Can I use a PPP loan to pay independent contractors?

Nope. Your 1099 workers will have to apply for their own PPP loans beginning April 10th. Their wages CANNOT be included in the calculation of your ‘Average Monthly Payroll Costs.’

If I don’t have employees…can I use PPP to pay myself?

UPDATE (04.09.20 9:01am): After completing my own PPP application via my bank (US Bank) I have updated and clarified a few details below.

UPDATE (04.10.20 3:15pm): Further clarifications provided below regarding formal payroll vs 1099-MISC income.

- If you have received income solely via 1099-MISC this CAN be used to qualify your “Average Monthly Payroll Costs” to determine the amount for your loan.

- If you paid yourself a regular monthly W-2 salary you can use PPP to cover your own payroll at the rate of 2.5x your monthly salary.

E.g. If your average monthly salary is $5000, you’ll receive a PPP “loan” of $12,500.

- If you paid yourself monthly shareholder distributions and did one yearly payroll check (as most S-corp owners do), you should still qualify for your PPP loan. This is my circumstance and my application so far has gone through. But I have yet to submit payroll documentation, so the verdict is still out for those of us who process one yearly payroll check.

Can I apply for PPP AND Unemployment?

Nope. Can’t double-dip (to my knowledge…but honestly I can’t verify this anywhere). Calculate which will earn you more overall benefits and determine the best option. Or simply see who’s website works and let’s you apply???

Can I apply for PPP, EIDL, AND get my grant?

Yes, you are eligible to receive your “up-to” $10,000 EIDL grant and still apply for a PPP loan. In addition you can even apply for both an EIDL loan AND a PPP loan with the only stipulation being that you don’t use the funds from each loan for the same expenses6.

When will I get my money?

According to Investopedia7:

After you submit your application you will be assigned a loan officer. The quicker you respond to any questions they have, the faster your application will be processed. You should receive your loan advance within days of successfully filing your application. The EIDL loan will take longer and, since this involves an unprecedented amount of money over the entire country, it will likely take longer than usual.

To summarize…Nobody. Flippin’. Knows.

Section 4: Filing For Unemployment Insurance (UI)

If you are either a W-2 employee or an independent contractor who’s not eligible for either the EIDL loan or the PPP program, you’ve ended up here.

To clarify: You CANNOT earn benefits from either of these loan programs AND simultaneously draw unemployment benefits (as of writing this article, at least).

Income Potential:

An EXTRA $600/week (in ADDITION TO your existing benefits) for up to 4 EXTRA months

If you primarily earn your income as an employee via W-2, you are most likely already familiar with the process of applying for unemployment (and liken it to root canal as I do).

If you primarily earn your income as a freelancer or independent contractor via 1099 income, up until the CARES Act was passed, you were S.O.L.

But now (in theory) you are FINALLY amongst the elite who have access to unemployment!!!!!

Well….that is of course when it actually works.

Here’s a comprehensive FAQ List regarding the current state of California EDD

My hope is that by the time you read this article many of the above statements are all obsolete and freelancers nationwide have access to the proper forms to apply for unemployment.

UPDATE 04.10.20 03:19pm: If you live in California, EDD has now sent clarification about increased benefits payments and how to apply as an independent contractor. See below.

Who is eligible?

While regulations will vary on a state-by-state basis (unemployment is not a federal program), here are the basic stipulations for independent contractors:

If you are self-employed, an independent contractor, or gig worker and are unable to work or have had your hours reduced due to COVID-19, you may be eligible for Unemployment Insurance (UI) benefits under a few different scenarios:

- You chose to contribute to UI Elective Coverage and paid the required contributions to be considered potentially eligible for benefits.

- Your past employer made contributions on your behalf over the past 5 to 18 months.

- You may have been misclassified as an independent contractor instead of an employee.

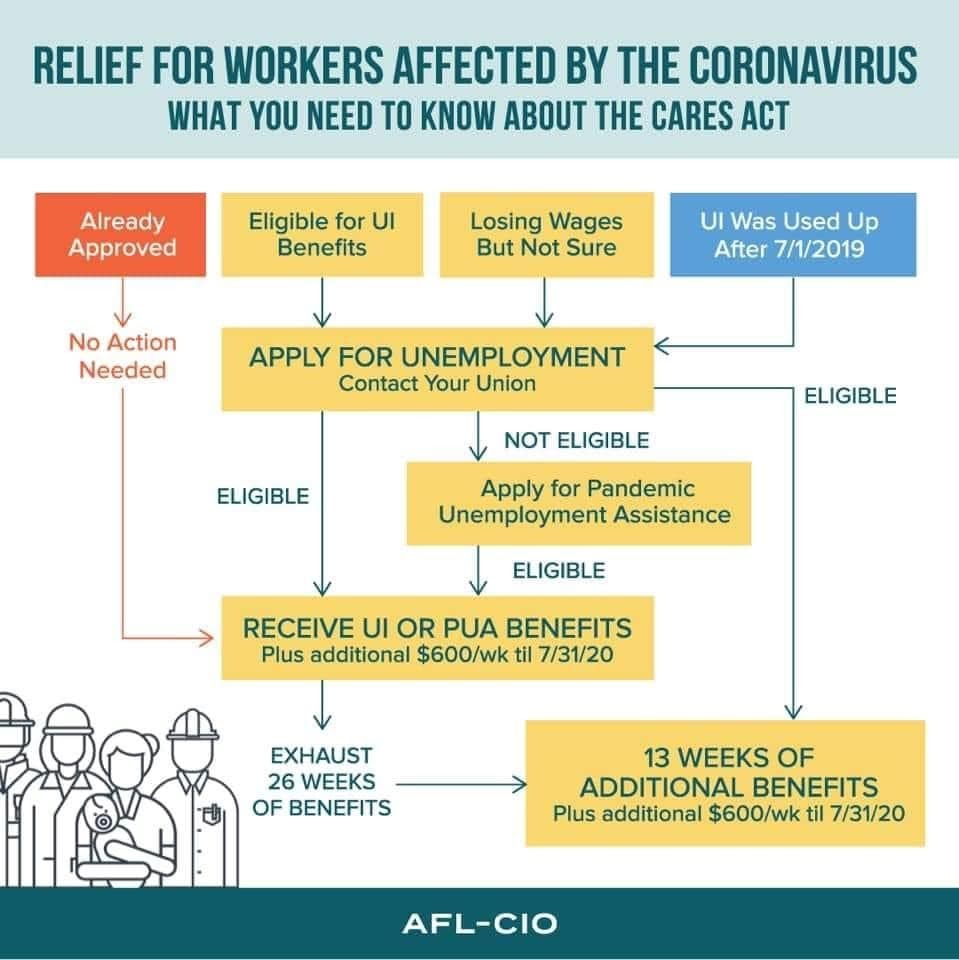

Here is a helpful flowchart to understand how to proceed based on your current unemployment status:

Where do I apply as a freelancer?

While this will vary state by state, if you live in California, here’s the brand new web portal with the latest updates about applying for EDD as an independent contractor.

What additional benefits can I receive?

As per the CARES Act, regardless of the state you live in:

- You will receive an additional $600 per week on top of whatever existing benefits you would be eligible for (based on your previous income).

- You will receive up to four months of extra benefits

- They have also waived the one-week waiting period (although at this point this is most likely moot as just about everyone has already lost their jobs)

When will I get my benefits?

As mentioned above, this process is currently a mess…especially in California. Some states have opened up applications for freelancers and some haven’t.

If you were already receiving benefits as a W2 employee, or if you recently applied for benefits, according to this announcement (published 04.10.10) you will see your increased benefits after claiming for the week ending April 11th, 2020.

In short, based on the way unemployment generally works, assume you’ll get your first check 2-3 weeks after your application is processed.

Once it’s processed…..

Section 5: Other Ways to Earn Income

Once you’ve maximized all of your available income options from federal and state programs…what now?

Aside from refreshing your online bank account every 15 minutes to ensure your benefits (eventually) arrive, it might appear there are no other options to generate income. After all, nobody has any idea how long present circumstances will last, how long we’ll be ‘safer at home,’ and when the job market will open (and cameras roll) again.

Perhaps now is the time to acknowledge how dependent your livelihood is on other people’s ideas & projects?

Maybe now is the time to start developing your own ideas?

Write that script?

Develop that pitch?

Edit that sizzle reel for YOUR show idea?

Start your podcast?

Write the first draft of your book?

Or perhaps it’s FINALLY time to take your random side-hustle idea seriously?

I’ve talked to numerous people in my coaching & mentorship community who have said that this pandemic has given them a newfound perspective on how much (or how little) they actually enjoy what they do for a living and how dependent they are on others to survive.

If you’d like to explore ideas for starting your own online business so you are in control of your income and no longer dependent on outside projects to survive, the Earnable program is my #1 recommendation for starting your online business. This is where I began 5 years ago, and it’s the most comprehensive step-by-step program for anyone who wants to start their own business, regardless of whether or not you even have an idea right now.

What’s Next…

Now that you’ve organized & prioritized your expenses in Part 1 of this series…

And now that you’ve maximized your various options for income in Part 2 of this series by doing one (or several) of the following:

- Calculating Your Stimulus Check

- Applying for Your SBA Disaster Loan (and grant)

- Applying for Paycheck Protection

- Applying for Unemployment Insurance

In Part 3 of this series (publishing soon) I’ll show you step-by-step how to reorganize your financial workflow so you can fully automate your finances, set money aside for the next emergency (or global pandemic), and rest easy during that next hiatus knowing you’ve bought yourself plenty of time before you need the next paycheck.

Zack Arnold

Zack Arnold (ACE) is an award-winning Hollywood film editor & producer (Cobra Kai, Empire, Burn Notice, Unsolved, Glee), a documentary director, father of 2, an American Ninja Warrior, and the creator of Optimize Yourself. He believes we all deserve to love what we do for a living...but not at the expense of our health, our relationships, or our sanity. He provides the education, motivation, and inspiration to help ambitious creative professionals DO better and BE better. “Doing” better means learning how to more effectively manage your time and creative energy so you can produce higher quality work in less time. “Being” better means doing all of the above while still prioritizing the most important people and passions in your life…all without burning out in the process. Click to download Zack’s “Ultimate Guide to Optimizing Your Creativity (And Avoiding Burnout).”